000170364412/312024Q2FALSE33.33xbrli:sharesiso4217:USDxbrli:pureiso4217:USDxbrli:sharesgpmt:segmentgpmt:loan00017036442024-01-012024-06-300001703644us-gaap:CommonStockMember2024-01-012024-06-300001703644us-gaap:SeriesAPreferredStockMember2024-01-012024-06-3000017036442024-07-3100017036442024-06-3000017036442023-12-310001703644us-gaap:SeriesAPreferredStockMember2023-01-012023-12-310001703644us-gaap:SeriesAPreferredStockMember2024-06-300001703644us-gaap:SeriesAPreferredStockMember2023-12-310001703644us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2024-06-300001703644us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-3100017036442024-04-012024-06-3000017036442023-04-012023-06-3000017036442023-01-012023-06-300001703644us-gaap:CommonStockMember2022-12-310001703644us-gaap:PreferredStockMember2022-12-310001703644us-gaap:AdditionalPaidInCapitalMember2022-12-310001703644us-gaap:RetainedEarningsMember2022-12-310001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2022-12-310001703644us-gaap:ParentMember2022-12-310001703644us-gaap:NoncontrollingInterestMember2022-12-3100017036442022-12-310001703644us-gaap:RetainedEarningsMember2023-01-012023-03-310001703644us-gaap:ParentMember2023-01-012023-03-3100017036442023-01-012023-03-310001703644us-gaap:CommonStockMember2023-01-012023-03-310001703644us-gaap:AdditionalPaidInCapitalMember2023-01-012023-03-310001703644us-gaap:CumulativePreferredStockMember2023-01-012023-03-310001703644us-gaap:CumulativePreferredStockMemberus-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-01-012023-03-310001703644us-gaap:ParentMemberus-gaap:CumulativePreferredStockMember2023-01-012023-03-310001703644us-gaap:SeriesAPreferredStockMember2023-01-012023-03-310001703644us-gaap:SeriesAPreferredStockMemberus-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-01-012023-03-310001703644us-gaap:ParentMemberus-gaap:SeriesAPreferredStockMember2023-01-012023-03-310001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-01-012023-03-310001703644us-gaap:CommonStockMember2023-03-310001703644us-gaap:PreferredStockMember2023-03-310001703644us-gaap:AdditionalPaidInCapitalMember2023-03-310001703644us-gaap:RetainedEarningsMember2023-03-310001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-03-310001703644us-gaap:ParentMember2023-03-310001703644us-gaap:NoncontrollingInterestMember2023-03-3100017036442023-03-310001703644us-gaap:RetainedEarningsMember2023-04-012023-06-300001703644us-gaap:ParentMember2023-04-012023-06-300001703644us-gaap:AdditionalPaidInCapitalMember2023-04-012023-06-300001703644us-gaap:CumulativePreferredStockMember2023-04-012023-06-300001703644us-gaap:CumulativePreferredStockMemberus-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-04-012023-06-300001703644us-gaap:ParentMemberus-gaap:CumulativePreferredStockMember2023-04-012023-06-300001703644us-gaap:SeriesAPreferredStockMember2023-04-012023-06-300001703644us-gaap:SeriesAPreferredStockMemberus-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-04-012023-06-300001703644us-gaap:ParentMemberus-gaap:SeriesAPreferredStockMember2023-04-012023-06-300001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-04-012023-06-300001703644us-gaap:CommonStockMember2023-04-012023-06-300001703644us-gaap:CommonStockMember2023-06-300001703644us-gaap:PreferredStockMember2023-06-300001703644us-gaap:AdditionalPaidInCapitalMember2023-06-300001703644us-gaap:RetainedEarningsMember2023-06-300001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-06-300001703644us-gaap:ParentMember2023-06-300001703644us-gaap:NoncontrollingInterestMember2023-06-3000017036442023-06-300001703644us-gaap:CommonStockMember2023-12-310001703644us-gaap:PreferredStockMember2023-12-310001703644us-gaap:AdditionalPaidInCapitalMember2023-12-310001703644us-gaap:RetainedEarningsMember2023-12-310001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-12-310001703644us-gaap:ParentMember2023-12-310001703644us-gaap:NoncontrollingInterestMember2023-12-310001703644us-gaap:RetainedEarningsMember2024-01-012024-03-310001703644us-gaap:ParentMember2024-01-012024-03-3100017036442024-01-012024-03-310001703644us-gaap:AdditionalPaidInCapitalMember2024-01-012024-03-310001703644us-gaap:SeriesAPreferredStockMember2024-01-012024-03-310001703644us-gaap:SeriesAPreferredStockMemberus-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2024-01-012024-03-310001703644us-gaap:ParentMemberus-gaap:SeriesAPreferredStockMember2024-01-012024-03-310001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2024-01-012024-03-310001703644us-gaap:CommonStockMember2024-01-012024-03-310001703644us-gaap:CommonStockMember2024-03-310001703644us-gaap:PreferredStockMember2024-03-310001703644us-gaap:AdditionalPaidInCapitalMember2024-03-310001703644us-gaap:RetainedEarningsMember2024-03-310001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2024-03-310001703644us-gaap:ParentMember2024-03-310001703644us-gaap:NoncontrollingInterestMember2024-03-3100017036442024-03-310001703644us-gaap:RetainedEarningsMember2024-04-012024-06-300001703644us-gaap:ParentMember2024-04-012024-06-300001703644us-gaap:CommonStockMember2024-04-012024-06-300001703644us-gaap:AdditionalPaidInCapitalMember2024-04-012024-06-300001703644us-gaap:SeriesAPreferredStockMember2024-04-012024-06-300001703644us-gaap:SeriesAPreferredStockMemberus-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2024-04-012024-06-300001703644us-gaap:ParentMemberus-gaap:SeriesAPreferredStockMember2024-04-012024-06-300001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2024-04-012024-06-300001703644us-gaap:CommonStockMember2024-06-300001703644us-gaap:PreferredStockMember2024-06-300001703644us-gaap:AdditionalPaidInCapitalMember2024-06-300001703644us-gaap:RetainedEarningsMember2024-06-300001703644us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2024-06-300001703644us-gaap:ParentMember2024-06-300001703644us-gaap:NoncontrollingInterestMember2024-06-300001703644us-gaap:BuildingMember2024-06-300001703644us-gaap:LandImprovementsMember2024-06-300001703644us-gaap:FirstMortgageMember2024-06-300001703644us-gaap:JuniorLoansMember2024-06-300001703644us-gaap:FirstMortgageMember2024-01-012024-06-300001703644us-gaap:JuniorLoansMember2024-01-012024-06-300001703644us-gaap:FirstMortgageMember2023-12-310001703644us-gaap:JuniorLoansMember2023-12-310001703644us-gaap:FirstMortgageMember2023-01-012023-12-310001703644us-gaap:JuniorLoansMember2023-01-012023-12-3100017036442023-01-012023-12-310001703644srt:OfficeBuildingMember2024-06-300001703644srt:OfficeBuildingMember2023-12-310001703644srt:MultifamilyMember2024-06-300001703644srt:MultifamilyMember2023-12-310001703644srt:HotelMember2024-06-300001703644srt:HotelMember2023-12-310001703644srt:RetailSiteMember2024-06-300001703644srt:RetailSiteMember2023-12-310001703644srt:IndustrialPropertyMember2024-06-300001703644srt:IndustrialPropertyMember2023-12-310001703644srt:OtherPropertyMember2024-06-300001703644srt:OtherPropertyMember2023-12-310001703644gpmt:UnitedStatesNortheasternRegionMember2024-06-300001703644gpmt:UnitedStatesNortheasternRegionMember2023-12-310001703644gpmt:UnitedStatesSouthwesternRegionMember2024-06-300001703644gpmt:UnitedStatesSouthwesternRegionMember2023-12-310001703644gpmt:UnitedStatesWesternRegionMember2024-06-300001703644gpmt:UnitedStatesWesternRegionMember2023-12-310001703644gpmt:UnitedStatesMidwesternRegionMember2024-06-300001703644gpmt:UnitedStatesMidwesternRegionMember2023-12-310001703644gpmt:UnitedStatesSoutheasternRegionMember2024-06-300001703644gpmt:UnitedStatesSoutheasternRegionMember2023-12-310001703644gpmt:LoansTrancheOneMember2024-04-012024-06-300001703644gpmt:LoansTrancheThreeMember2024-04-012024-06-300001703644gpmt:LoansTrancheOneMember2024-01-012024-06-300001703644gpmt:LoansTrancheThreeMember2024-01-012024-06-300001703644us-gaap:OtherLiabilitiesMemberus-gaap:UnfundedLoanCommitmentMember2024-01-012024-06-300001703644us-gaap:UnfundedLoanCommitmentMember2024-06-300001703644us-gaap:UnfundedLoanCommitmentMember2024-04-012024-06-300001703644us-gaap:UnfundedLoanCommitmentMember2024-01-012024-06-300001703644us-gaap:CollateralPledgedMember2024-06-300001703644gpmt:TenLoansMemberus-gaap:FairValueMeasurementsNonrecurringMember2024-06-300001703644srt:OfficeBuildingMemberus-gaap:AssetPledgedAsCollateralMember2024-06-300001703644us-gaap:AssetPledgedAsCollateralMembergpmt:MixedUsePropertyMember2024-06-300001703644srt:HotelMemberus-gaap:AssetPledgedAsCollateralMember2024-06-300001703644srt:MultifamilyMemberus-gaap:AssetPledgedAsCollateralMember2024-06-300001703644us-gaap:CollateralPledgedMembersrt:OfficeBuildingMember2024-06-300001703644srt:OfficeBuildingMembergpmt:TwoLoansMemberus-gaap:FairValueMeasurementsNonrecurringMember2024-06-300001703644gpmt:NonAccrualLoanMember2024-06-300001703644us-gaap:FairValueMeasurementsNonrecurringMembergpmt:TwelveLoansMember2024-06-300001703644us-gaap:FairValueMeasurementsNonrecurringMembergpmt:NonAccrualLoanMembergpmt:ThirteenLoansMember2024-06-300001703644gpmt:NonAccrualLoanMember2023-06-300001703644us-gaap:FairValueMeasurementsNonrecurringMembergpmt:FourLoansMember2023-06-300001703644gpmt:FiveLoansMemberus-gaap:FairValueMeasurementsNonrecurringMembergpmt:NonAccrualLoanMember2023-06-300001703644us-gaap:FirstMortgageMember2024-04-012024-06-300001703644gpmt:SeniorLoanMember2024-04-012024-06-300001703644us-gaap:UnfundedLoanCommitmentMember2024-04-012024-06-300001703644gpmt:MezzanineNoteMember2024-04-012024-06-300001703644us-gaap:FirstMortgageMember2024-06-300001703644us-gaap:FirstMortgageMember2023-12-310001703644gpmt:RiskRating1Member2024-06-300001703644gpmt:RiskRating1Member2023-12-310001703644gpmt:RiskRating2Member2024-06-300001703644gpmt:RiskRating2Member2023-12-310001703644gpmt:RiskRating3Member2024-06-300001703644gpmt:RiskRating3Member2023-12-310001703644gpmt:RiskRating4Member2024-06-300001703644gpmt:RiskRating4Member2023-12-310001703644gpmt:RiskRating5Member2024-06-300001703644gpmt:RiskRating5Member2023-12-310001703644gpmt:RiskRating5Member2024-04-012024-06-300001703644us-gaap:InterestRateRiskMember2024-04-012024-06-300001703644gpmt:RiskRating5Membersrt:OfficeBuildingMember2024-04-012024-06-300001703644gpmt:CommercialMortgageLoanMemberus-gaap:UnlikelyToBeCollectedFinancingReceivableMembergpmt:OfficePhoenixAZMember2023-05-160001703644gpmt:CommercialMortgageLoanMembergpmt:OfficePhoenixAZMember2023-05-160001703644gpmt:OfficePhoenixAZMember2023-05-160001703644gpmt:CommercialMortgageLoanMemberus-gaap:UnlikelyToBeCollectedFinancingReceivableMembergpmt:OfficeMaynardMAMember2024-06-270001703644gpmt:CommercialMortgageLoanMembergpmt:OfficeMaynardMAMember2024-06-270001703644gpmt:OfficeMaynardMAMember2024-06-270001703644gpmt:OfficePhoenixAZMembergpmt:TenantImprovementsMember2024-01-012024-06-300001703644gpmt:OfficePhoenixAZMemberus-gaap:LeasesAcquiredInPlaceMember2024-01-012024-06-300001703644gpmt:AboveMarketLeaseMembergpmt:OfficePhoenixAZMember2024-01-012024-06-300001703644gpmt:BelowMarketLeaseMembergpmt:OfficePhoenixAZMember2024-01-012024-06-300001703644gpmt:GPMT2021FL4CRECLOMembergpmt:CollateralAssetsMember2024-06-300001703644gpmt:GPMT2021FL4CRECLOMembergpmt:CollateralAssetsMember2023-12-310001703644gpmt:FinancingProvidedMembergpmt:GPMT2021FL4CRECLOMember2024-06-300001703644gpmt:FinancingProvidedMembergpmt:GPMT2021FL4CRECLOMember2023-12-310001703644gpmt:CollateralAssetsMembergpmt:GPMT2021FL3CRECLOMember2024-06-300001703644gpmt:CollateralAssetsMembergpmt:GPMT2021FL3CRECLOMember2023-12-310001703644gpmt:FinancingProvidedMembergpmt:GPMT2021FL3CRECLOMember2024-06-300001703644gpmt:FinancingProvidedMembergpmt:GPMT2021FL3CRECLOMember2023-12-310001703644gpmt:CollateralAssetsMember2024-06-300001703644gpmt:CollateralAssetsMember2023-12-310001703644gpmt:FinancingProvidedMember2024-06-300001703644gpmt:FinancingProvidedMember2023-12-310001703644gpmt:LenderMorganStanleyBankMemberus-gaap:LoansReceivableMember2024-06-300001703644gpmt:LenderGoldmanSachsBankMemberus-gaap:LoansReceivableMember2024-06-300001703644gpmt:LenderJPMorganChaseBankMemberus-gaap:LoansReceivableMember2024-06-300001703644us-gaap:LoansReceivableMembergpmt:LenderCitibankMember2024-06-300001703644us-gaap:SecuredDebtMember2024-06-300001703644gpmt:LenderMorganStanleyBankMemberus-gaap:LoansReceivableMember2023-12-310001703644gpmt:LenderGoldmanSachsBankMemberus-gaap:LoansReceivableMember2023-12-310001703644gpmt:LenderJPMorganChaseBankMemberus-gaap:LoansReceivableMember2023-12-310001703644us-gaap:LoansReceivableMembergpmt:LenderCitibankMember2023-12-310001703644gpmt:CentennialCorporateFinanceGroupMemberus-gaap:LoansReceivableMember2023-12-310001703644us-gaap:SecuredDebtMember2023-12-310001703644us-gaap:RevolvingCreditFacilityMemberus-gaap:AssetPledgedAsCollateralMember2023-12-310001703644gpmt:RepurchaseAgreementCounterpartyMorganStanleyBankMember2024-06-300001703644gpmt:RepurchaseAgreementCounterpartyMorganStanleyBankMember2024-01-012024-06-300001703644gpmt:RepurchaseAgreementCounterpartyMorganStanleyBankMember2023-12-310001703644gpmt:RepurchaseAgreementCounterpartyMorganStanleyBankMember2023-01-012023-12-310001703644gpmt:RepurchaseAgreementCounterpartyJPMorganChaseBankMember2024-06-300001703644gpmt:RepurchaseAgreementCounterpartyJPMorganChaseBankMember2024-01-012024-06-300001703644gpmt:RepurchaseAgreementCounterpartyJPMorganChaseBankMember2023-12-310001703644gpmt:RepurchaseAgreementCounterpartyJPMorganChaseBankMember2023-01-012023-12-310001703644gpmt:RepurchaseAgreementCounterpartyGoldmanSachsBankMember2024-06-300001703644gpmt:RepurchaseAgreementCounterpartyGoldmanSachsBankMember2024-01-012024-06-300001703644gpmt:RepurchaseAgreementCounterpartyGoldmanSachsBankMember2023-12-310001703644gpmt:RepurchaseAgreementCounterpartyGoldmanSachsBankMember2023-01-012023-12-310001703644gpmt:RepurchaseAgreementCounterpartyCitibankMember2024-06-300001703644gpmt:RepurchaseAgreementCounterpartyCitibankMember2024-01-012024-06-300001703644gpmt:RepurchaseAgreementCounterpartyCitibankMember2023-12-310001703644gpmt:RepurchaseAgreementCounterpartyCitibankMember2023-01-012023-12-310001703644gpmt:RepurchaseAgreementCounterpartyCentennialCorporateFinanceGroupMember2024-06-300001703644gpmt:RepurchaseAgreementCounterpartyCentennialCorporateFinanceGroupMember2023-12-310001703644gpmt:RepurchaseAgreementCounterpartyCentennialCorporateFinanceGroupMember2023-01-012023-12-310001703644srt:MaximumMember2024-06-300001703644gpmt:DebtCovenantPeriodOneMember2024-06-300001703644gpmt:DebtCovenantPeriodTwoMember2024-06-300001703644us-gaap:ConvertibleDebtMembergpmt:ConvertibleDebt2018IssuanceMember2018-10-310001703644gpmt:ConvertibleDebt2018IssuanceMember2023-12-310001703644gpmt:ConvertibleDebt2018IssuanceMember2024-06-300001703644gpmt:ConvertibleSeniorNotesMember2024-04-012024-06-300001703644gpmt:ConvertibleSeniorNotesMember2023-04-012023-06-300001703644gpmt:ConvertibleSeniorNotesMember2024-01-012024-06-300001703644gpmt:ConvertibleSeniorNotesMember2023-01-012023-06-300001703644us-gaap:AssetPledgedAsCollateralMembergpmt:NonCommercialRealEstateCollateralizedMortgageObligationsFinancingActivitiesMember2024-06-300001703644us-gaap:AssetPledgedAsCollateralMembergpmt:NonCommercialRealEstateCollateralizedMortgageObligationsFinancingActivitiesMember2023-12-310001703644gpmt:CollateralDependentLoansMembergpmt:ElevenLoansMember2024-06-300001703644gpmt:ElevenLoansMemberus-gaap:FairValueMeasurementsNonrecurringMember2024-06-300001703644gpmt:CollateralDependentLoansMemberus-gaap:ValuationTechniqueDiscountedCashFlowMembergpmt:NineLoansMember2024-06-300001703644us-gaap:ValuationTechniqueDiscountedCashFlowMembergpmt:NineLoansMemberus-gaap:FairValueMeasurementsNonrecurringMember2024-06-300001703644srt:MinimumMembergpmt:LoanOneMembergpmt:MeasurementInputExitCapitalizationRateMember2024-06-300001703644gpmt:LoanOneMembersrt:MaximumMembergpmt:MeasurementInputExitCapitalizationRateMember2024-06-300001703644srt:MinimumMembergpmt:LoanOneMemberus-gaap:MeasurementInputDiscountRateMember2024-06-300001703644gpmt:LoanOneMemberus-gaap:MeasurementInputDiscountRateMembersrt:MaximumMember2024-06-300001703644gpmt:CollateralDependentLoansMembergpmt:TwoLoansMember2024-06-300001703644us-gaap:FairValueMeasurementsNonrecurringMembergpmt:TwoLoansMember2024-06-300001703644gpmt:PublicOfferingMemberus-gaap:SeriesAPreferredStockMember2021-11-302021-12-100001703644gpmt:PublicOfferingMember2021-11-302021-12-100001703644us-gaap:SeriesAPreferredStockMemberus-gaap:OverAllotmentOptionMember2022-01-182022-02-080001703644srt:MinimumMember2024-01-012024-06-300001703644srt:MaximumMember2024-01-012024-06-300001703644us-gaap:SeriesAPreferredStockMember2023-01-012023-06-300001703644us-gaap:SeriesAPreferredStockMembergpmt:SubREITMember2021-01-310001703644us-gaap:SeriesAPreferredStockMember2021-01-310001703644us-gaap:SeriesAPreferredStockMembergpmt:SubREITMember2021-01-012021-01-310001703644us-gaap:CommonStockMember2024-06-182024-06-180001703644us-gaap:CommonStockMember2024-03-142024-03-140001703644us-gaap:CommonStockMember2023-06-222023-06-220001703644us-gaap:CommonStockMember2023-03-162023-03-160001703644us-gaap:CommonStockMember2023-01-012023-06-300001703644gpmt:ShareRepurchaseProgramMember2023-05-090001703644gpmt:ShareRepurchaseProgramMember2023-01-012023-06-300001703644gpmt:ShareRepurchaseProgramMember2023-04-012023-06-300001703644gpmt:ShareRepurchaseProgramMember2024-01-012024-06-300001703644gpmt:ShareRepurchaseProgramMember2024-04-012024-06-300001703644gpmt:RepurchasedSharesFromEmployeesMember2023-01-012023-06-300001703644us-gaap:PreferredStockMember2024-06-182024-06-180001703644us-gaap:PreferredStockMember2024-03-142024-03-140001703644us-gaap:PreferredStockMember2024-01-012024-06-300001703644us-gaap:PreferredStockMember2023-06-222023-06-220001703644us-gaap:PreferredStockMember2023-03-162023-03-160001703644us-gaap:PreferredStockMember2023-01-012023-06-300001703644gpmt:A2022PlanMember2024-06-300001703644us-gaap:RestrictedStockUnitsRSUMember2023-12-310001703644us-gaap:PerformanceSharesMember2023-12-310001703644us-gaap:RestrictedStockUnitsRSUMember2024-01-012024-03-310001703644us-gaap:PerformanceSharesMember2024-01-012024-03-310001703644us-gaap:RestrictedStockUnitsRSUMember2024-03-310001703644us-gaap:PerformanceSharesMember2024-03-310001703644us-gaap:RestrictedStockUnitsRSUMember2024-04-012024-06-300001703644us-gaap:PerformanceSharesMember2024-04-012024-06-300001703644us-gaap:RestrictedStockUnitsRSUMember2024-06-300001703644us-gaap:PerformanceSharesMember2024-06-300001703644gpmt:PerformanceSharesGrantedIn2021Member2024-06-300001703644gpmt:YearOneMemberus-gaap:RestrictedStockUnitsRSUMember2024-01-012024-06-300001703644gpmt:YearOneMemberus-gaap:PerformanceSharesMember2024-01-012024-06-300001703644gpmt:YearOneMember2024-01-012024-06-300001703644gpmt:YearTwoMemberus-gaap:RestrictedStockUnitsRSUMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMembergpmt:YearTwoMember2024-01-012024-06-300001703644gpmt:YearTwoMember2024-01-012024-06-300001703644gpmt:YearThreeMemberus-gaap:RestrictedStockUnitsRSUMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMembergpmt:YearThreeMember2024-01-012024-06-300001703644gpmt:YearThreeMember2024-01-012024-06-300001703644gpmt:YearFourMemberus-gaap:RestrictedStockUnitsRSUMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMembergpmt:YearFourMember2024-01-012024-06-300001703644gpmt:YearFourMember2024-01-012024-06-300001703644us-gaap:RestrictedStockMember2023-01-012023-06-300001703644us-gaap:RestrictedStockUnitsRSUMember2024-01-012024-06-300001703644us-gaap:RestrictedStockUnitsRSUMember2023-04-012023-06-300001703644us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-06-300001703644us-gaap:PerformanceSharesMembersrt:MinimumMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMembersrt:MaximumMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2024-01-012024-06-300001703644us-gaap:ShareBasedCompensationAwardTrancheThreeMemberus-gaap:PerformanceSharesMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMembergpmt:ShareBasedPaymentArrangementTrancheFourMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMembergpmt:ShareBasedPaymentArrangementTrancheFiveMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMembergpmt:ShareBasedPaymentArrangementTrancheSixMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMember2024-01-012024-06-300001703644us-gaap:PerformanceSharesMember2023-04-012023-06-300001703644us-gaap:PerformanceSharesMember2023-01-012023-06-300001703644us-gaap:ConvertibleDebtMember2023-04-012023-06-300001703644us-gaap:RestrictedStockUnitsRSUMember2024-04-012024-06-300001703644us-gaap:RestrictedStockUnitsRSUMember2024-01-012024-06-300001703644us-gaap:SubsequentEventMemberus-gaap:FirstMortgageMember2024-07-012024-08-050001703644us-gaap:SubsequentEventMembergpmt:SeniorLoanMember2024-07-012024-08-050001703644us-gaap:UnfundedLoanCommitmentMemberus-gaap:SubsequentEventMember2024-07-012024-08-050001703644us-gaap:SubsequentEventMembergpmt:MezzanineNoteMember2024-07-012024-08-050001703644us-gaap:SubsequentEventMemberus-gaap:FirstMortgageMember2024-08-05

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| | | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2024

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-38124

GRANITE POINT MORTGAGE TRUST INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Maryland | | 61-1843143 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | | | | | | | | | |

3 Bryant Park, Suite 2400A | | |

| New York, | New York | | 10036 |

| (Address of principal executive offices) | | (Zip Code) |

(212) 364-5500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | | GPMT | | NYSE |

| 7.00% Series A Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock, par value $0.01 per share | | GPMTPrA | | NYSE |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | | Accelerated filer | ☒ |

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

As of July 31, 2024, there were 50,684,117 shares of outstanding common stock, par value $0.01 per share, issued and outstanding.

GRANITE POINT MORTGAGE TRUST INC.

INDEX

| | | | | | | | |

| | Page |

| PART I - FINANCIAL INFORMATION | |

Item 1. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART II - OTHER INFORMATION | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains, or incorporates by reference, not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and that are subject to the safe harbors created by such sections. Forward-looking statements involve numerous risks and uncertainties. Our actual results may differ from our beliefs, expectations, estimates and projections and, consequently, you should not rely on these forward-looking statements as predictions of future events. Forward-looking statements are not historical in nature and can be identified by words such as “anticipate,” “estimate,” “will,” “should,” “expect,” “target,” “believe,” “outlook,” “potential,” “continue,” “intend,” “seek,” “plan,” “goals,” “future,” “likely,” “may” and similar expressions or their negative forms, or by references to strategy, plans or intentions. By their nature, forward-looking statements speak only as of the date they are made, are not statements of historical facts or guarantees of future performance and are subject to risks, uncertainties, assumptions or changes in circumstances that are difficult to predict or quantify. Our expectations, beliefs and estimates are expressed in good faith and we believe there is a reasonable basis for them. However, there can be no assurance that management's expectations, beliefs and estimates will prove to be correct or be achieved and actual results may vary materially from what is expressed in or indicated by the forward-looking statements.

These forward-looking statements are subject to risks and uncertainties, including, among other things, those described in our Annual Report on Form 10-K for the year ended December 31, 2023, under the caption “Risk Factors.” Other risks, uncertainties and factors that could cause actual results to differ materially from those projected are described below and may be described from time to time in reports we file with the Securities and Exchange Commission, or the SEC, including our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update or revise any such forward-looking statements, whether as a result of new information, future events or otherwise.

Important factors that may affect our actual results include, among others:

•the general political, economic and competitive conditions in the markets in which we invest and their impact on our investment portfolio, financial condition and business operations;

•inflationary trends which have led to higher interest rates and increased market volatility;

•reduced demand for office, multifamily or retail space, including as a result of increased hybrid work schedules which allow work from remote locations other than the employer's office premises;

•defaults by borrowers in paying debt service on outstanding indebtedness and borrowers' abilities to manage and stabilize properties;

•our ability to obtain or maintain financing arrangements on terms favorable to us or at all;

•the level and volatility of prevailing interest rates and credit spreads;

•reductions in the yield on our investments and increases in the cost of our financing;

•general volatility of the securities markets in which we participate and the potential need to post additional collateral on our financing arrangements;

•the return or impact of current or future investments;

•changes in our business, investment strategies or target investments;

•increased competition from entities investing in our target investments;

•effects of hedging instruments on our target investments;

•changes in governmental regulations, tax law and rates and similar matters;

•our ability to maintain our qualification as a real estate investment trust, or REIT, for U.S. federal income tax purposes and our exclusion from registration under the Investment Company Act of 1940, as amended, or the Investment Company Act;

•availability of desirable investment opportunities;

•threats to information security, including by way of cyber-attacks;

•availability of qualified personnel;

•operational failures by third-parties on whom we rely in the conduct of our business;

•estimates relating to our ability to make distributions to our stockholders in the future;

•natural disasters, such as hurricanes, earthquakes, wildfires and floods, including climate change-related risks; acts of war and/or terrorism; pandemics or outbreaks of infectious disease; and other events that may cause unanticipated and uninsured performance declines and/or losses to us or the owners and operators of the real estate securing our investments;

•deterioration in the performance of the properties securing our investments that may cause deterioration in the performance of our investments, risks in collection of contractual interest payments and, potentially, principal losses to us, including the risk of credit loss charges and any impact on our ability to satisfy the covenants and conditions in our debt agreements; and

•difficulty or delays in redeploying the proceeds from repayments of our existing investments.

This Quarterly Report on Form 10-Q may contain statistics and other data that, in some cases, have been obtained or compiled from information made available by loan servicers and other third-party service providers.

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements (unaudited)

GRANITE POINT MORTGAGE TRUST INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except share data)

| | | | | | | | | | | |

| June 30,

2024 | | December 31,

2023 |

| ASSETS | | | |

| Loans held-for-investment | $ | 2,616,884 | | | $ | 2,718,486 | |

| Allowance for credit losses | (264,140) | | | (134,661) | |

| Loans held-for-investment, net | 2,352,744 | | | 2,583,825 | |

| | | |

| | | |

| | | |

| Cash and cash equivalents | 85,916 | | | 188,370 | |

| Restricted cash | 12,880 | | | 10,846 | |

| Real estate owned, net | 42,820 | | | 16,939 | |

| Accrued interest receivable | 10,725 | | | 12,380 | |

| | | |

| | | |

| | | |

| Other assets | 41,666 | | | 34,572 | |

Total Assets (1) | $ | 2,546,751 | | | $ | 2,846,932 | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | |

| Liabilities | | | |

| Repurchase facilities | $ | 791,556 | | | $ | 875,442 | |

| Securitized debt obligations | 938,075 | | | 991,698 | |

| | | |

| Secured credit facility | 85,192 | | | 84,000 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Dividends payable | 6,335 | | | 14,136 | |

| Other liabilities | 20,892 | | | 22,633 | |

Total Liabilities (1) | 1,842,050 | | | 1,987,909 | |

Commitments and Contingencies (see Note 10) | | | |

| | | |

| Stockholders’ Equity | | | |

7.00% Series A cumulative redeemable preferred stock, par value $0.01 per share; 11,500,000 shares authorized, and 8,229,500 and 8,229,500 shares issued and outstanding, respectively; liquidation preference $25.00 per share | 82 | | | 82 | |

Common stock, par value $0.01 per share; 450,000,000 shares authorized, and 50,684,117 shares and 50,577,841 issued and outstanding, respectively | 507 | | | 506 | |

| Additional paid-in capital | 1,198,894 | | | 1,198,048 | |

| Cumulative earnings | (69,696) | | | 67,495 | |

| Cumulative distributions to stockholders | (425,211) | | | (407,233) | |

| Total Granite Point Mortgage Trust Inc. Stockholders’ Equity | 704,576 | | | 858,898 | |

| Non-controlling interests | 125 | | | 125 | |

| Total Equity | 704,701 | | | 859,023 | |

| Total Liabilities and Stockholders’ Equity | $ | 2,546,751 | | | $ | 2,846,932 | |

______________________

(1)The condensed consolidated balance sheets include assets of consolidated variable interest entities, or VIEs, that can only be used to settle obligations of these VIEs, and liabilities of the consolidated VIEs for which creditors do not have recourse to Granite Point Mortgage Trust Inc. At June 30, 2024, and December 31, 2023, assets of the VIEs totaled $1,101,207 and $1,233,821, respectively, and liabilities of the VIEs totaled $939,878 and $994,081, respectively. See Note 5 - Variable Interest Entities and Securitized Debt Obligations, for further detail.

The accompanying notes are an integral part of these condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME

(in thousands, except share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Six Months Ended |

| | June 30, | | June 30, |

| | 2024 | | 2023 | | 2024 | | 2023 | | |

| Interest income: | | | |

| Loans held-for-investment | $ | 46,882 | | | $ | 66,217 | | | $ | 98,847 | | | $ | 131,508 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Cash and cash equivalents | 1,597 | | | 2,609 | | | 3,687 | | | 4,037 | | | |

| Total interest income | 48,479 | | | 68,826 | | | 102,534 | | | 135,545 | | | |

| Interest expense: | | | | | | | | | |

| Repurchase facilities | 19,331 | | | 22,872 | | | 40,059 | | | 42,644 | | | |

| Secured credit facility | 2,714 | | | 3,075 | | | 5,403 | | | 6,004 | | | |

| Securitized debt obligations | 18,303 | | | 17,888 | | | 36,418 | | | 35,939 | | | |

| Convertible senior notes | — | | | 2,332 | | | — | | | 4,643 | | | |

| | | | | | | | | | |

| Asset-specific financings | — | | | 819 | | | — | | | 1,562 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Total interest expense | 40,348 | | | 46,986 | | | 81,880 | | | 90,792 | | | |

| Net interest income | 8,131 | | | 21,840 | | | 20,654 | | | 44,753 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Other income (loss): | | | | | | | | | |

| Revenue from real estate owned operations | 1,111 | | | 462 | | | 2,253 | | | 462 | | | |

| | | | | | | | | | |

| Provision for credit losses | (60,756) | | | (5,818) | | | (136,308) | | | (52,228) | | | |

| Gain (loss) on extinguishment of debt | (786) | | | — | | | (786) | | | 238 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Total other loss | (60,431) | | | (5,356) | | | (134,841) | | | (51,528) | | | |

| Expenses: | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Compensation and benefits | 4,721 | | | 6,209 | | | 10,708 | | | 12,121 | | | |

| Servicing expenses | 1,398 | | | 1,320 | | | 2,774 | | | 2,698 | | | |

| Expenses from real estate owned operations | 1,950 | | | 1,664 | | | 3,995 | | | 1,664 | | | |

| Other operating expenses | 2,700 | | | 2,180 | | | 5,529 | | | 5,451 | | | |

| | | | | | | | | | |

| Total expenses | 10,769 | | | 11,373 | | | 23,006 | | | 21,934 | | | |

| (Loss) income before income taxes | (63,069) | | | 5,111 | | | (137,193) | | | (28,709) | | | |

| (Benefit from) provision for income taxes | (1) | | | 70 | | | (2) | | | 79 | | | |

| Net (loss) income | (63,068) | | | 5,041 | | | (137,191) | | | (28,788) | | | |

| Dividends on preferred stock | 3,600 | | | 3,625 | | | 7,200 | | | 7,250 | | | |

| | | | | | | | | | |

| Net (loss) income attributable to common stockholders | $ | (66,668) | | | $ | 1,416 | | | $ | (144,391) | | | $ | (36,038) | | | |

| Basic (loss) earnings per weighted average common share | $ | (1.31) | | | $ | 0.03 | | | $ | (2.84) | | | $ | (0.69) | | | |

| Diluted (loss) earnings per weighted average common share | $ | (1.31) | | | $ | 0.03 | | | $ | (2.84) | | | $ | (0.69) | | | |

| | | | | | | | | | |

| Weighted average number of shares of common stock outstanding: | | | | | | | | | |

| Basic | 50,939,476 | | | 51,538,309 | | | 50,842,004 | | | 51,921,217 | | | |

| Diluted | 50,939,476 | | | 51,619,072 | | | 50,842,004 | | | 51,921,217 | | | |

| | | | | | | | | | |

| Net (loss) income attributable to common stockholders | $ | (66,668) | | | $ | 1,416 | | | $ | (144,391) | | | $ | (36,038) | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Comprehensive (loss) income | $ | (66,668) | | | $ | 1,416 | | | $ | (144,391) | | | $ | (36,038) | | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(in thousands, except share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Preferred Stock | | | | | | | | | | | | | | | | |

| Shares | | Amount | | Shares | | Amount | | Additional Paid-in Capital | | | | | | Cumulative Earnings | | Cumulative Distributions to Stockholders | | Total Stockholders’ Equity | | Non-controlling Interests | | Total Equity |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Balance, December 31, 2022 | 52,350,989 | | | $ | 524 | | | 8,229,500 | | | $ | 82 | | | $ | 1,202,315 | | | | | | | $ | 130,693 | | | $ | (350,069) | | | $ | 983,545 | | | $ | 125 | | | $ | 983,670 | |

| Net (loss) income | — | | | — | | | — | | | — | | | — | | | | | | | (33,829) | | | — | | | (33,829) | | | — | | | (33,829) | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Repurchase of common stock | (1,001,338) | | | (10) | | | — | | | — | | | (5,108) | | | | | | | — | | | — | | | (5,118) | | | — | | | (5,118) | |

| Restricted stock forfeiture | (36,916) | | | (1) | | | — | | | — | | | (236) | | | | | | | — | | | — | | | (237) | | | — | | | (237) | |

| Restricted Stock Unit (RSU) forfeiture | — | | | — | | | — | | | — | | | (652) | | | | | | | — | | | — | | | (652) | | | — | | | (652) | |

Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (25) | | | (25) | | | — | | | (25) | |

Preferred dividends declared, $0.4375 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (3,600) | | | (3,600) | | | — | | | (3,600) | |

Common dividends declared, $0.20 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (10,706) | | | (10,706) | | | — | | | (10,706) | |

| Non-cash equity award compensation | 213,304 | | | 2 | | | — | | | — | | | 1,953 | | | | | | | — | | | — | | | 1,955 | | | — | | | 1,955 | |

| Balance, March 31, 2023 | 51,526,039 | | | $ | 515 | | | 8,229,500 | | | $ | 82 | | | $ | 1,198,272 | | | | | | | $ | 96,864 | | | $ | (364,400) | | | $ | 931,333 | | | $ | 125 | | | $ | 931,458 | |

| Net income | — | | | — | | | — | | | — | | | — | | | | | | | 5,041 | | | — | | | 5,041 | | | — | | | 5,041 | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Restricted Stock Unit (RSU) forfeiture | — | | | — | | | — | | | — | | | (77) | | | | | | | — | | | — | | | (77) | | | — | | | (77) | |

Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (25) | | | (25) | | | — | | | (25) | |

Preferred dividends declared, $0.4375 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (3,600) | | | (3,600) | | | — | | | (3,600) | |

Common dividends declared, $0.20 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (10,736) | | | (10,736) | | | — | | | (10,736) | |

| Non-cash equity award compensation | 44,664 | | | 1 | | | — | | | — | | | 2,385 | | | | | | | — | | | — | | | 2,386 | | | — | | | 2,386 | |

| Balance, June 30, 2023 | 51,570,703 | | | 516 | | | 8,229,500 | | | 82 | | | 1,200,580 | | | | | | | 101,905 | | | (378,761) | | | 924,322 | | | 125 | | | 924,447 | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Balance, December 31, 2023 | 50,577,841 | | | $ | 506 | | | 8,229,500 | | | $ | 82 | | | $ | 1,198,048 | | | | | | | $ | 67,495 | | | $ | (407,233) | | | $ | 858,898 | | | $ | 125 | | | $ | 859,023 | |

| Net (loss) income | — | | | — | | | — | | | — | | | — | | | | | | | (74,123) | | | — | | | (74,123) | | | — | | | (74,123) | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Restricted Stock Unit (RSU) forfeiture | — | | | — | | | — | | | — | | | (1,185) | | | | | | | — | | | — | | | (1,185) | | | — | | | (1,185) | |

| | | | | | | | | | | | | | | | | | | | | | | |

Preferred dividends declared, $0.4375 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (3,600) | | | (3,600) | | | — | | | (3,600) | |

Common dividends declared, $0.15 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (8,043) | | | (8,043) | | | — | | | (8,043) | |

| Non-cash equity award compensation | 456,959 | | | 4 | | | — | | | — | | | 2,167 | | | | | | | — | | | — | | | 2,171 | | | — | | | 2,171 | |

| Balance, March 31, 2024 | 51,034,800 | | | $ | 510 | | | 8,229,500 | | | $ | 82 | | | $ | 1,199,030 | | | | | | | $ | (6,628) | | | $ | (418,876) | | | $ | 774,118 | | | $ | 125 | | | $ | 774,243 | |

| Net (loss) income | — | | | — | | | — | | | — | | | — | | | | | | | (63,068) | | | — | | | (63,068) | | | — | | | (63,068) | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Repurchase of common stock | (510,244) | | | (5) | | | — | | | — | | | (1,594) | | | | | | | — | | | — | | | (1,599) | | | — | | | (1,599) | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

Preferred dividends declared, $0.4375 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (3,600) | | | (3,600) | | | — | | | (3,600) | |

Common dividends declared, $0.05 per share | — | | | — | | | — | | | — | | | — | | | | | | | — | | | (2,735) | | | (2,735) | | | — | | | (2,735) | |

| Non-cash equity award compensation | 159,561 | | | 2 | | | — | | | — | | | 1,458 | | | | | | | — | | | — | | | 1,460 | | | — | | | 1,460 | |

| Balance, June 30, 2024 | 50,684,117 | | | $ | 507 | | | 8,229,500 | | | $ | 82 | | | $ | 1,198,894 | | | | | | | $ | (69,696) | | | $ | (425,211) | | | $ | 704,576 | | | $ | 125 | | | $ | 704,701 | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (in thousands) | | | | | | | | | | | | | | |

| | |

| | Six Months Ended June 30, |

| | 2024 | | 2023 | | |

| Cash Flows From Operating Activities: | | | |

| Net loss | $ | (137,191) | | | $ | (28,788) | | | |

| Adjustments to reconcile net (loss) income to net cash provided by operating activities: | | | | | |

| Accretion of discounts and net deferred fees on loans held-for-investment and deferred interest capitalized to loans held-for-investment | (3,453) | | | (5,854) | | | |

| Amortization of deferred debt issuance costs | 3,316 | | | 4,333 | | | |

| Provision for credit losses | 136,308 | | | 52,228 | | | |

| (Gain) loss on extinguishment of debt | 423 | | | (274) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Amortization of equity-based compensation | 3,631 | | | 4,341 | | | |

| | | | | | |

| Depreciation and amortization on real estate owned | 2,558 | | | — | | | |

| Net change in assets and liabilities: | | | | | |

| Decrease (increase) in accrued interest receivable | 1,655 | | | 216 | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Decrease (increase) in other assets | (2,088) | | | 999 | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Increase (decrease) in other liabilities | (2,521) | | | (810) | | | |

| | | | | | |

| Net cash provided by operating activities | 2,638 | | | 26,391 | | | |

| Cash Flows From Investing Activities: | | | | | |

| Originations, acquisitions and additional fundings of loans held-for-investment, net of deferred fees | (34,053) | | | (34,318) | | | |

| | | | | | |

| | | | | | |

| Proceeds from repayment of loans held-for-investment | 96,883 | | | 265,623 | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Net cash provided by (used in) investing activities | 62,830 | | | 231,305 | | | |

| | | | | | |

| Cash Flows From Financing Activities: | | | | | |

| Proceeds from repurchase facilities | 78,486 | | | 453,242 | | | |

| Principal payments on repurchase facilities | (161,949) | | | (396,676) | | | |

| | | | | | |

| Principal payments on securitized debt obligations | (54,210) | | | (139,215) | | | |

| | | | | | |

| | | | | | |

| Proceeds from asset-specific financings | — | | | 911 | | | |

| | | | | | |

| Proceeds from secured credit facility | 1,192 | | | — | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Payment of debt issuance costs | (843) | | | (3,514) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Tax withholding on restricted stock and RSUs | (1,185) | | | (966) | | | |

| Repurchase of common stock | (1,599) | | | (5,118) | | | |

| Redemption of cumulative redeemable preferred stock | — | | | (1,000) | | | |

| Dividends paid on preferred stock | (7,201) | | | (7,251) | | | |

| Dividends paid on common stock | (18,579) | | | (21,424) | | | |

| Net cash (used in) provided by financing activities | (165,888) | | | (121,011) | | | |

| Net (decrease) increase in cash, cash equivalents and restricted cash | (100,420) | | | 136,685 | | | |

| Cash, cash equivalents, and restricted cash at beginning of period | 199,216 | | | 140,165 | | | |

| Cash, cash equivalents, and restricted cash at end of period | $ | 98,796 | | | $ | 276,850 | | | |

| Supplemental Disclosure of Cash Flow Information: | | | | | |

| Cash paid for interest | $ | 83,764 | | | $ | 90,379 | | | |

| | | | | | |

| Cash paid for taxes | $ | — | | | $ | 697 | | | |

| Noncash Activities: | | | | | |

| | | | | | |

| Dividends declared but not paid at end of period | $ | 6,335 | | | $ | 14,336 | | | |

| Transfers from loans held-for-investment to real estate owned, other assets and other liabilities | $ | 35,659 | | | $ | 24,000 | | | |

| | | | | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements

Note 1. Organization and Operations

Granite Point Mortgage Trust Inc., or the Company, is an internally managed commercial real estate finance company that focuses primarily on directly originating, investing in and managing senior floating-rate commercial mortgage loans and other debt and debt-like commercial real estate investments. These investments are capitalized by accessing a variety of funding sources, including borrowing under the Company’s bank credit facilities or other asset financings, issuing commercial real estate collateralized loan obligations, or CRE CLOs, and issuing other forms of secured and unsecured debt and equity securities, depending on market conditions and the Company’s view of the most appropriate funding option available for the Company’s investments. The Company is not in the business of buying or trading securities, and the only securities it owns are the retained interests from its CRE CLOs. The Company’s investment objective is to preserve the Company’s stockholders’ capital while generating attractive risk-adjusted returns over the long term, primarily through dividends derived from current income produced by the Company’s investment portfolio. The Company’s common stock is listed on the NYSE under the symbol “GPMT”. The Company operates its business in a manner that is intended to permit it to maintain its exclusion from registration under the Investment Company Act of 1940. The Company operates its business as one segment. The Company was incorporated in Maryland on April 7, 2017, and commenced operations as a publicly traded company on June 28, 2017.

The Company has elected to be treated as a REIT, as defined under the Internal Revenue Code of 1986, as amended, or the Code, for U.S. federal income tax purposes. As long as the Company continues to comply with a number of requirements under federal tax law and maintains its qualification as a REIT, the Company generally will not be subject to U.S. federal income taxes to the extent that the Company distributes its taxable income to its stockholders on an annual basis and does not engage in prohibited transactions. However, certain activities that the Company may perform may cause it to earn income which will not be qualifying income for REIT purposes. The Company has designated one of its subsidiaries as a taxable REIT subsidiary, or TRS, as defined in the Code, to engage in such activities.

Note 2. Basis of Presentation and Significant Accounting Policies

Consolidation and Basis of Presentation

The interim unaudited condensed consolidated financial statements of the Company have been prepared in accordance with the rules and regulations of the SEC. Certain information and note disclosures normally included in financial statements prepared in accordance with U.S. generally accepted accounting principles, or U.S. GAAP, have been condensed or omitted according to such SEC rules and regulations. However, management believes that the disclosures included in these interim condensed consolidated financial statements are adequate to make the information presented not misleading. The accompanying unaudited condensed consolidated financial statements should be read in conjunction with the financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023. In the opinion of management, all normal and recurring adjustments necessary to present fairly the financial condition of the Company at June 30, 2024, and results of operations for all periods presented have been made. The results of operations for the three and six months ended June 30, 2024, should not be construed as indicative of the results to be expected for future periods or the full year.

The unaudited condensed consolidated financial statements of the Company include the accounts of all subsidiaries; inter-company accounts and transactions have been eliminated.

All entities in which the Company holds investments that are considered variable interest entities, or VIEs, for financial reporting purposes were reviewed for consolidation under the applicable consolidation guidance. Whenever the Company has both the power to direct the activities of an entity that most significantly impact the entity’s performance, and the obligation to absorb losses or the right to receive benefits of the entity that could be significant, the Company consolidates the entity. See Note 5 - Variable Interest Entities and Securitized Debt Obligations to the Company’s Condensed Consolidated Financial Statements included in this Quarterly Report on Form 10-Q for additional details regarding consolidation of VIEs.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make a number of significant estimates. These include estimates of amount and timing of allowances for credit losses, fair value of certain assets and liabilities, and other estimates that affect the reported amounts of certain assets and liabilities as of the date of the condensed consolidated financial statements and the reported amounts of certain revenues and expenses during the reported period. It is likely that changes in these estimates (e.g., valuation changes to the underlying collateral of loans due to changes in market interest and capitalization rates, leasing, credit-worthiness of major tenants, occupancy rates, availability of financing, exit plan, loan sponsorship, actions of other lenders, overall economic and capital markets conditions, the broader commercial real estate market, local geographic sub-markets or other factors) will occur in the near term.

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements

The Company believes the estimates and assumptions underlying its condensed consolidated financial statements are reasonable and supportable based on the information available as of June 30, 2024. However, the Company’s actual results could ultimately differ from its estimates and such differences may be material.

Significant Accounting Policies

Included in Note 2 to the Consolidated Financial Statements of the Company’s Annual Report on Form 10-K for the year ended December 31, 2023, is a summary of the Company’s significant accounting policies. Provided below is a summary of additional accounting policies that are significant to the Company’s condensed consolidated financial condition and results of operations for the three and six months ended June 30, 2024.

Real Estate Owned

As part of its portfolio management strategy to maximize an economic outcome from a defaulted loan, the Company may assume legal title or physical possession of the underlying collateral property through foreclosure or the execution of a deed-in-lieu of foreclosure. Real estate acquired through a foreclosure or by deed-in-lieu of foreclosure is classified as real estate owned, or REO. The Company’s basis in REO and related acquired assets is equal to the estimated fair value of the collateral on the acquisition date and allocated within Real estate owned, Other assets and Other liabilities on the Company’s condensed consolidated balance sheets. The estimated fair value of REO is determined using generally accepted valuation techniques, including a discounted cash flow model and inputs that include the highest and best use for each asset, estimated future values based on discussions with local brokers, investors and other market participants, the estimated holding period for the asset, and discount rates that reflect estimated investor return requirements for the risks associated with the expected use of each asset. If the estimated fair value of REO is lower than the carrying value of the related loan upon acquisition, the difference is recorded through the provision for credit losses in the Company’s condensed consolidated statements of comprehensive income. Upon acquisition, the Company allocates the fair value of REO to land and land improvements, building and building improvements, tenant improvements, intangible assets and intangible liabilities, as applicable.

As of June 30, 2024, REO and related acquired assets, except for land, are depreciated using the straight-line method over estimated useful lives as follows:

| | | | | | | | |

| Description | | Depreciable Life |

| Building | | 39 years |

| Land improvements | | 15 Years |

| Tenant improvements | | Over lease terms |

| Lease intangibles | | Over lease terms |

Renovations and/or replacements that improve or extend the life of the REO are capitalized and depreciated over their estimated useful lives. The cost of ordinary repairs and maintenance are expensed as incurred in the Company’s condensed consolidated statements of comprehensive income.

REO is initially measured at fair value and is thereafter subject to an impairment assessment on a quarterly basis. Subsequent to a REO acquisition, events or circumstances may occur that may result in a material and sustained decrease in the cash flows generated from the property. REO is evaluated for recoverability when impairment indicators are identified. Any impairment losses and gains or losses on sale are included in the Company’s condensed consolidated statements of comprehensive income. Revenue and expenses from REO operations are included in the condensed consolidated statements of comprehensive income within Revenue from real estate owned operations and Expenses from real estate owned operations, as applicable.

Recently Issued and/or Adopted Accounting Standards

Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures

In November 2023, the FASB issued ASU 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures, or ASU 2023-07. The new guidance requires a public entity with a single reportable segment to provide new disclosures surrounding segment expenses and other segment items on an annual and interim basis, with the intention of improving reportable segment disclosure requirements as well as enhancing interim disclosure requirements. ASU 2023-07 is effective for fiscal years beginning after December 15, 2023, and for interim periods with fiscal years beginning after December 15, 2024, with the guidance to be adopted retrospectively to all prior periods presented. The Company is currently evaluating the impact of this guidance but does not anticipate it will have a material impact on the Company’s condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements

Income Taxes (Topic 740): Improvements to Income Tax Disclosures

In December 2023, the FASB issued ASU 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures, or ASU 2023-09. The new guidance requires entities to disclose the amount of income taxes paid, net of refunds received, disaggregated by federal, state and foreign jurisdiction, with the intention of improving the transparency of income tax disclosures. ASU 2023-09 is effective for fiscal years beginning after December 15, 2024, and is to be adopted on a prospective basis with the option to apply retrospectively. The Company is currently evaluating the impact of this guidance but does not anticipate it will have a material impact on the Company’s condensed consolidated financial statements.

Note 3. Loans Held-for-Investment, Net of Allowance for Credit Losses

The following tables summarize the Company’s loans held-for-investment by asset type, property type and geographic location as of June 30, 2024, and December 31, 2023:

| | | | | | | | | | | | | | | | | | | |

| June 30, 2024 |

| (dollars in thousands) | Senior Loans(1) | | | | B-Notes(2) | | Total |

| Unpaid principal balance | $ | 2,610,510 | | | | | $ | 13,374 | | | $ | 2,623,884 | |

Unamortized (discount) premium | (5) | | | | | — | | | (5) | |

Unamortized net deferred origination fees | (6,995) | | | | | — | | | (6,995) | |

| Allowance for credit losses | (263,868) | | | | | (272) | | | (264,140) | |

| Carrying value | $ | 2,339,642 | | | | | $ | 13,102 | | | $ | 2,352,744 | |

| Unfunded commitments | $ | 118,010 | | | | | $ | — | | | $ | 118,010 | |

| Number of loans | 67 | | | | | 1 | | | 68 | |

Weighted average coupon(3) | 7.0 | % | | | | 8.0 | % | | 7.0 | % |

Weighted average years to maturity(4) | 0.4 | | | | 2.6 | | 0.4 |

| | | | | | | | | | | | | | | | | | | |

| December 31, 2023 |

| (dollars in thousands) | Senior Loans(1) | | | | B-Notes(2) | | Total |

| Unpaid principal balance | $ | 2,713,672 | | | | | $ | 13,507 | | | $ | 2,727,179 | |

Unamortized (discount) premium | (19) | | | | | — | | | (19) | |

Unamortized net deferred origination fees | (8,674) | | | | | — | | | (8,674) | |

| Allowance for credit losses | (134,302) | | | | | (359) | | | (134,661) | |

| Carrying value | $ | 2,570,677 | | | | | $ | 13,148 | | | $ | 2,583,825 | |

| Unfunded commitments | $ | 160,698 | | | | | $ | — | | | $ | 160,698 | |

| Number of loans | 72 | | | | | 1 | | | 73 | |

Weighted average coupon(3) | 8.2 | % | | | | 8.0 | % | | 8.2 | % |

Weighted average years to maturity(4) | 0.7 | | | | 3.1 | | 0.7 |

______________________

(1)Loans primarily secured by a first priority lien on commercial real property and related personal property and also includes, when applicable, any companion subordinate loans.

(2)A subordinate loan secured by the same mortgage as the senior loan.

(3)Weighted average coupon inclusive of the impact of nonaccrual loans.

(4)Based on contractual maturity date, including maturity defaulted loans with no remaining term. Certain loans are subject to contractual extension options with such conditions stipulated in the applicable loan documents. Actual maturities may differ from contractual maturities stated herein as certain borrowers may have the right to prepay with or without paying a prepayment fee. The Company may also extend contractual maturities in connection with certain loan modifications.

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (dollars in thousands) | | June 30, 2024 | | December 31, 2023 |

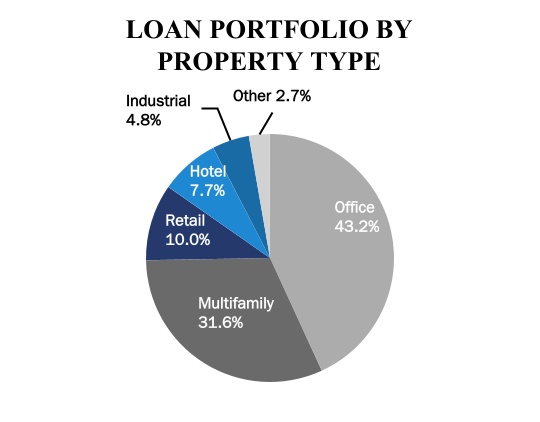

| Property Type | | Carrying Value | | % of Loan Portfolio | | Carrying Value | | % of Loan Portfolio |

| Office | | $ | 1,015,245 | | | 43.2 | % | | $ | 1,116,551 | | | 43.2 | % |

| Multifamily | | 742,615 | | | 31.6 | % | | 826,125 | | | 32.0 | % |

| Hotel | | 181,437 | | | 7.7 | % | | 180,891 | | | 7.0 | % |

| Retail | | 235,271 | | | 10.0 | % | | 257,945 | | | 10.0 | % |

| Industrial | | 114,060 | | | 4.8 | % | | 113,972 | | | 4.4 | % |

| Other | | 64,116 | | | 2.7 | % | | 88,341 | | | 3.4 | % |

| Total | | $ | 2,352,744 | | | 100.0 | % | | $ | 2,583,825 | | | 100.0 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (dollars in thousands) | | June 30, 2024 | | December 31, 2023 |

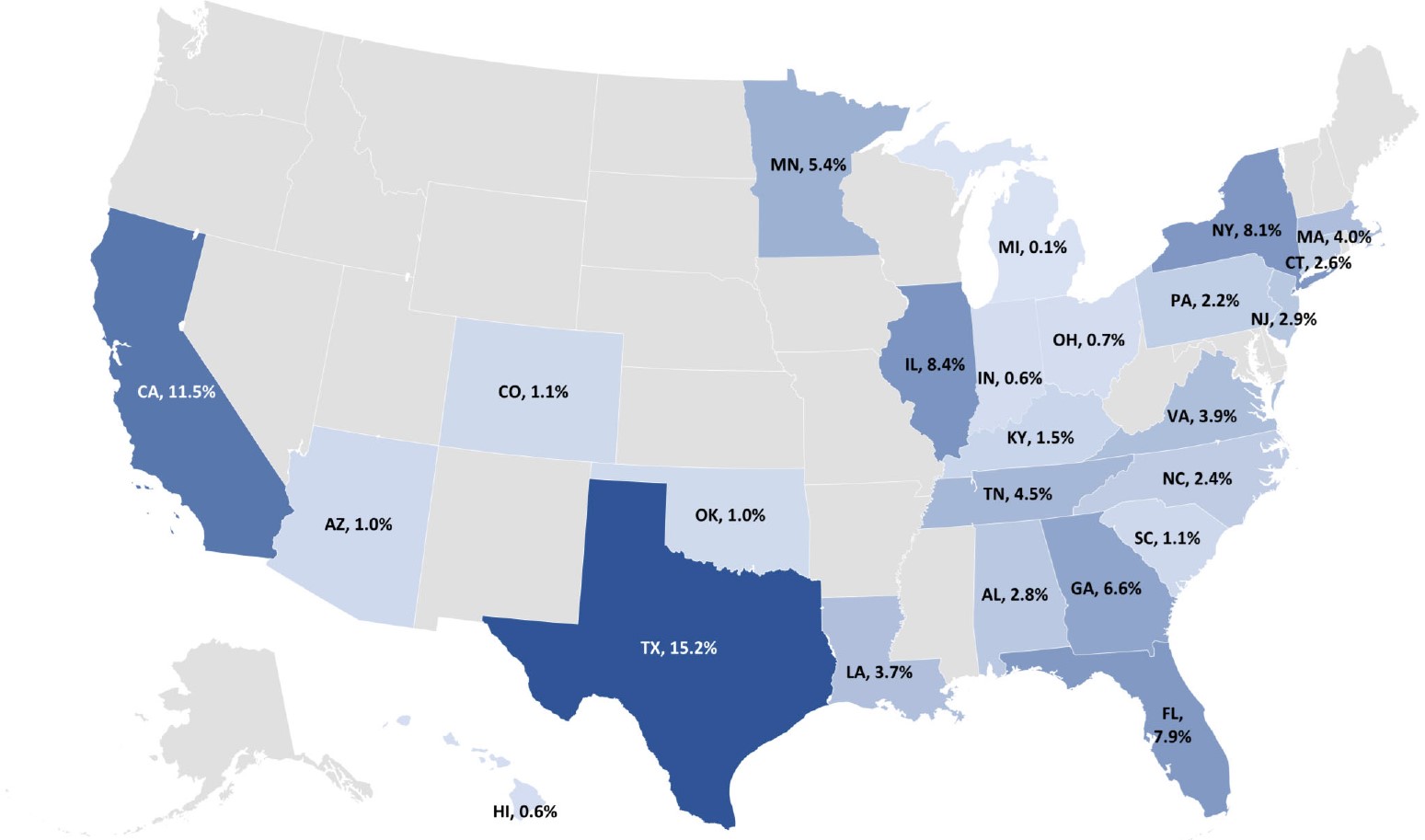

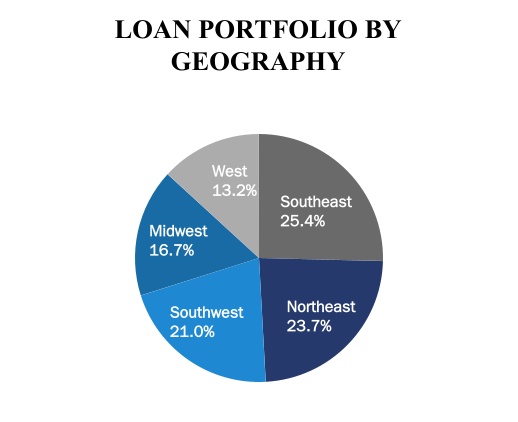

| Geographic Location | | Carrying Value | | % of Loan Portfolio | | Carrying Value | | % of Loan Portfolio |

| Northeast | | $ | 558,455 | | | 23.7 | % | | $ | 709,838 | | | 27.5 | % |

| Southwest | | 493,592 | | | 21.0 | % | | 495,133 | | | 19.2 | % |

| West | | 310,306 | | | 13.2 | % | | 328,547 | | | 12.7 | % |

| Midwest | | 392,773 | | | 16.7 | % | | 421,881 | | | 16.3 | % |

| Southeast | | 597,618 | | | 25.4 | % | | 628,426 | | | 24.3 | % |

| | | | | | | | |

| Total | | $ | 2,352,744 | | | 100.0 | % | | $ | 2,583,825 | | | 100.0 | % |

Loan Portfolio Activity

The following table summarizes activity related to loans held-for-investment, net of allowance for credit losses, for the three and six months ended June 30, 2024, and 2023:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| (in thousands) | | 2024 | | 2023 | | 2024 | | 2023 |

| Balance at beginning of period | | $ | 2,492,539 | | | $ | 3,182,379 | | | $ | 2,583,825 | | | $ | 3,267,815 | |

| Originations, additional fundings, upsizing of loans and capitalized deferred interest | | 17,867 | | | 18,975 | | | 35,868 | | | 37,180 | |

| | | | | | | | |

| Repayments | | (61,405) | | | (206,173) | | | (96,883) | | | (265,623) | |

| | | | | | | | |

| | | | | | | | |

| Transfers to real estate owned | | (35,659) | | | (24,000) | | | (35,659) | | | (24,000) | |

| Net discount accretion (premium amortization) | | 7 | | | 7 | | | 15 | | | 20 | |

| Increase (decrease) from net deferred origination fees | | (911) | | | (413) | | | (852) | | | (1,032) | |

| Amortization of net deferred origination fees | | 867 | | | 1,474 | | | 2,475 | | | 4,005 | |

| | | | | | | | |

| | | | | | | | |

| Provision for credit losses | | (60,561) | | | (6,161) | | | (136,045) | | | (52,277) | |

| Balance at end of period | | $ | 2,352,744 | | | $ | 2,966,088 | | | $ | 2,352,744 | | | $ | 2,966,088 | |

During the six months ended June 30, 2024, the Company funded $34.9 million of prior commitments and upsizings. Additionally, the Company received $67.7 million of full loan repayments, paydowns and amortization of $29.2 million, for total loan repayments, paydowns and amortization of $96.9 million.

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements

Allowance for Credit Losses

The following table presents the changes for the three and six months ended June 30, 2024, and 2023 in the allowance for credit losses on loans held-for-investment:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| (in thousands) | | 2024 | | 2023 | | 2024 | | 2023 |

| Balance at beginning of period | | $ | 210,145 | | | $ | 128,451 | | | $ | 134,661 | | | $ | 82,335 | |

| Provision for (benefit from) credit losses | | 60,561 | | | 6,161 | | | 136,045 | | | 52,277 | |

| Write-off | | (6,566) | | | (4,200) | | | (6,566) | | | (4,200) | |

| | | | | | | | |

| Balance at end of period | | $ | 264,140 | | | $ | 130,412 | | | $ | 264,140 | | | $ | 130,412 | |

During the three months ended June 30, 2024, the Company recorded a net increase of $54.0 million in its allowance for credit losses on loans held-for-investment. The increase was primarily due to: (i) $39.7 million related to loans that were individually assessed primarily driven by updated estimates of the fair value of the underlying collateral securing certain of these loans, and (ii) $14.3 million due to the ongoing challenges in the commercial real estate market and expectations for further pressure on property values and other loan specific assumptions employed in estimating the general Current Expected Credit Loss, or CECL, reserve.

During the six months ended June 30, 2024, the Company recorded a net increase of $129.5 million in its allowance for credit losses on loans held-for-investment. The increase was primarily due to: (i) $103.6 million related to eleven loans that were assessed individually and based on the estimates of the fair value of each loan’s underlying collateral, and (ii) $25.9 million due to the ongoing challenges in the commercial real estate market and expectations for further pressure on property values, and other loan specific assumptions employed in estimating the general CECL reserve.

As of June 30, 2024, the Company recognized $2.7 million in other liabilities related to the allowance for credit losses on unfunded commitments, resulting in a total allowance for credit losses of $266.9 million, and recorded a provision for credit losses of $(0.2) million and $(0.3) million for the three and six months ended June 30, 2024, respectively, partially offset by a decrease in unfunded commitments, resulting in a total provision for credit losses of $(60.8) million and $(136.3) million for the three and six months ended June 30, 2024, respectively.

As of June 30, 2024, the Company had ten collateral-dependent loans with an aggregate principal balance of $545.2 million, for which the Company recorded an allowance for credit losses of $195.0 million. These loans were individually assessed in accordance with the CECL framework and the allowance for credit losses was determined based on the estimates of the collateral properties’ fair value. The performance of the collateral properties securing these loans, which include four office buildings, four mixed-use properties with an office component, one hotel and one multifamily asset, has been impacted by an uncertain commercial real estate market and macroeconomic outlook, which includes weakening in credit fundamentals, capital markets volatility and significantly reduced real estate transaction activity, especially for certain property types, such as office assets located in underperforming markets, and a meaningfully higher cost of capital driven by high interest rates. These macroeconomic and market factors have resulted in the slowing of business plan execution and reduced market liquidity, thereby impacting the borrowers’ ability to either sell or refinance their properties to repay the Company’s loans. See Note 9 - Fair Value, for further detail on the fair value measurement of these loans.

Additionally, as of June 30, 2024, the Company had one collateral-dependent loan with an aggregate principal balance of $70.5 million secured by an office property, for which the Company recorded no allowance for credit losses as the collateral’s estimated fair value exceeded the loan balance. See Note 9 - Fair Value, for further detail on the fair value measurement of this loan.

Nonaccrual Loans

The following table presents the carrying value of loans held-for-investment on nonaccrual status for the three and six months ended June 30, 2024, and 2023:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| (in thousands) | | 2024 | | 2023 | | 2024 | | 2023 |

| Nonaccrual loan carrying value at beginning of period | | $ | 517,507 | | | $ | 207,234 | | | $ | 343,683 | | | $ | 207,958 | |

| Addition of nonaccrual loan carrying value | | 16,831 | | | — | | | 195,358 | | | 23,270 | |

| Reduction of nonaccrual loan carrying value | | (81,541) | | | (23,971) | | | (86,244) | | | (47,965) | |

| Nonaccrual loan carrying value at end of period | | $ | 452,797 | | | $ | 183,263 | | | $ | 452,797 | | | $ | 183,263 | |

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements

As of June 30, 2024, the Company had twelve senior loans with a total unpaid principal balance of $665.3 million and carrying value of $452.8 million that were held on nonaccrual status, compared to four senior loans with a total unpaid principal balance of $245.6 million and carrying value of $183.3 million that were held on nonaccrual status as of June 30, 2023. All other loans were considered current with respect to principal and interest payments due as of June 30, 2024, and June 30, 2023.

Loan Modifications